ZimVie - Undervalued MedTech spinoff

Post is originally from my previous blog www.globalstockpicking.com

Background

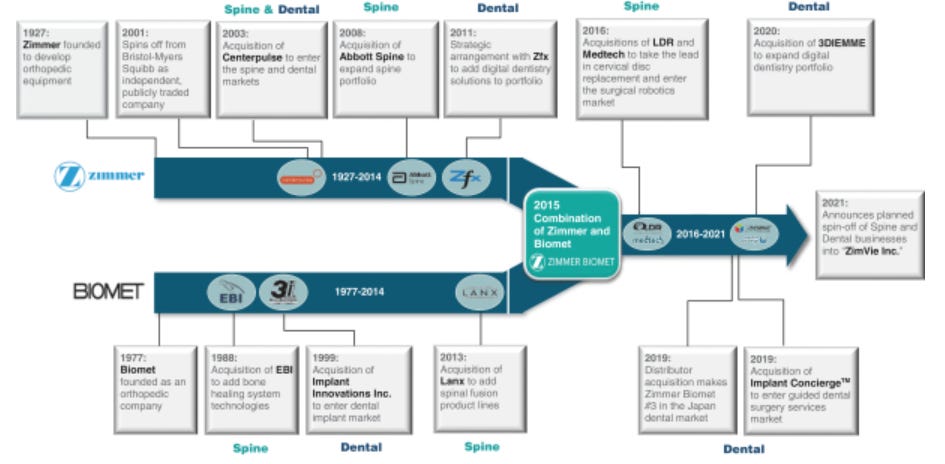

ZimVie completed it's spinoff from 29bn USD MCAP Zimmer Biomet (ZBH) in March 2022 and traded around a 800-700m MCAP + some 600m USD of debt after spinoff. The MCAP has since then shrunk to around below 150m USD and lately rebounded to 350m USD. The company is active in two segments: Dental (main product teeth implants) and Spine (main products spinal fusion and disc replacement).

Zimmer Biomet comes from a long history of spinoffs, mergers and acquisitions. Zimmer was spun off from Bristol-Myers Squibb in early 2000's. Including in the spinoff was the dental business which back then was a main segment within Zimmer (now part of ZimVie). In 2016 Zimmer Bio acquires LDR Holding for about 1bn USD, with the flagship product being Mobi-C artificial disc, which now belongs to ZimVie (current EV of ZimVie less than the Mobi-C purchase).

For industry background I made two post about the dental sector back in 2018: Dental Industry Part 1, Dental Industry Part 2 and one post in 2020 about how our spine health has worsened due to smartphone usage, strengthening the case for young people needing neck surgery: Smartphone usage – ticking time bomb.

ZimVie is a small company holding unique assets and in a unique position. To establish products on a global scale like ZimVie's has you need a massive sales network, this is something normally only large companies have the muscles to do. ZimVie coming from large Zimmer Bio has the benefit of being a small company but with that reach pre-established by a large company. Now the question is they can right size their business and leverage the advantaged they have. Press More to read the full story

Spinoff - Selling pressure gone

The spinoff was achieved through the distribution of 80.3% of the shares of ZimVie to holders of Zimmer Biomet common stock on March 1, 2022. The rest was initially held by Zimmer Bio. It's quite common that spinoffs perform poorly in its first year/years as a public company, firstly a big group of shareholders who usually only hold large caps are given a small cap position that they don't really want. This creates a huge selling pressure as they divest the spinoff they have been given. Secondly the company internally needs to find its feet, that can naturally take some time and in the meantime create some turbulence (this has clearly been the case with ZimVie). According to the 2023 proxy Zimmer Bio has disposed of its almost 20% position, most likely in blocks to some larger funds, like Camber Capital, a L/S hedge fund which now holds 10% of ZimVie's shares. This obviously also created significant selling pressure, which now seems to be done.

Why did Zimmer Biomet spin out its dental and spine segments? I have not come across any very clear explanation, but its clear that dental was a bit of an oddball in Zimmer Bio's large portfolio (totally different sales channels). Why then the motion preserving spine products was matched together with this is quite unclear. Spinning out the dental segment clearly made sense and given how bullish I am on the spine products ZimVie owns I am happy they paired these together, even though it doesn't fully make sense as the synergies is non-existing.

Management

Vafa Jamali a former Medtronic exec who oversaw the Zimmer competitor’s respiratory, gastrointestinal and informatics divisions, was selected to lead ZimVie in early 2021 (joined Zimmer Bio shortly after the spinoff plans were announced). He then worked roughly one year in Zimmer Bio before ZimVie was separated. His most recent role was as chief commercial officer of device maker Rockley Photonics and has not previously held the role of CEO elsewhere. Also the CFO was an external recruitment, there is continuity at the business segment level though, where Zimmer Biomet dental and spine business managers comes from Zimmer Bio and have joined ZimVie.

Glassdoor shows quite mixed reviews, some people are very positive whereas others are very bitter and says management is shit, hiring their buddies from outside etc. Trying to draw a balanced conclusion out of these comments, there seems to have been plenty of turbulence and pains trying to decouple from Zimmer Biomet and become a well oiled smaller separate company. This has also been confirmed to some degree by senior managers through various channels (conf calls, podcast etc).

Overall I rank management as one the areas of worry investing in ZimVie, unproven management that are steering a company with high debt and a tanking share price. Clearly they are off to a rough start.

Products / Market outlook

As previously introduced ZimVie is active in two segments: Dental and Spine. Below I will go a bit deeper into these two products and the outlook for the two segments.

Dental

The dental implant market is expected to have healthy growth over the foreseeable future. The global dental implants market reached a value of US$ 5.89 Billion in 2021. One market forecast expects this to reach US$ 7.64 Billion by 2027, a CAGR of 4.2%. Another forecast comments: "The globally rising senior population, which is especially prone to dental problems, is predicted to considerably contribute to market expansion" and predicted a 6.5% CAGR between 2023 and 2032.

Although implants for teeth is a very mature business with high competition among a number of players it has partly hit a new wave of growth thanks to digital technologies. Especially the usage of digital dental (intraoral) scanners has exploded and is becoming market standard. This together with 3d-printing has taken the dental prosthetics business into a new level of convenience and quality of outcomes. This is also seen in one of my other dental holdings, HK listed Modern Dental Group (3600.HK). ZimVie's dental business is global, with 50% in the US and 50% in Rest of the World (RoW).

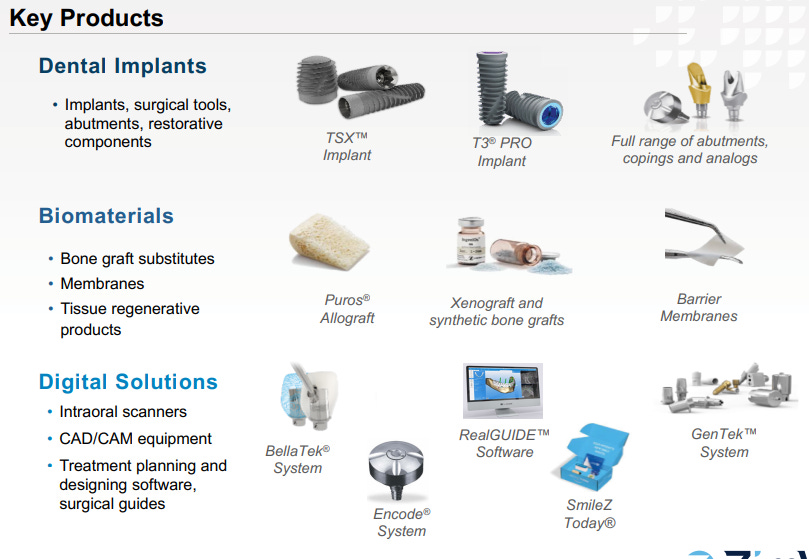

To be a successful seller of dental implants it has become essential to combine strong hardware with a strong digital product suite. My impression is that ZimVie (or previously Zimmer Bio) has been behind on the software side, with a quite outdated offering. This is evidenced by the acquisition done recently before the ZimVie spinoff of Italian company 3Diemme for about 30-40m USD (exact price tag not known). The company had developed a Cloud-based dental surgery workflow management solution for dentists. This acquisition seems to have translated into these new launches one year ago: ZimVie Announces Launch of the RealGUIDE™ CAD and FULL SUITE Software Modules. That said, I have not evaluated the difference software head-to-head, just based on my guess this specialist company are delivering a product in-line with competition (or perhaps even better than some, given its newly released). One can also think of this development as both a moat and a problem for a smaller company like ZimVie, previously you only had to provide solid "hardware", but now you need to also develop software to stay in the game, which is costly.

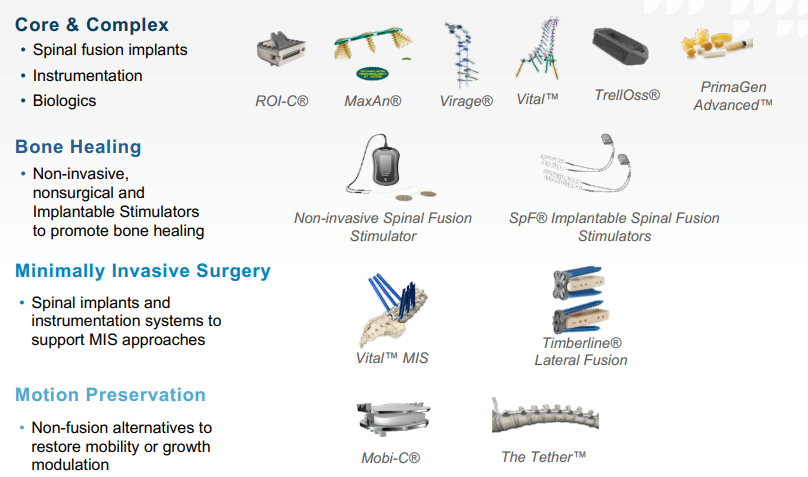

ZimVie key dental products

The T3-Pro which was launched one year ago is built on the previous T3 implant which has been used in more than 2 million implant procedures. So in the past year both the implant and the digital dentistry software has been improved upon, surely there has been major costs taken to get these across the finish-line. Given the tougher situation ZimVie is in given high debt etc (we will come back to this) it's good to note some large costs have already been taken to launch new generation products.

ZimVie dental market position

Since these are medical advanced products and procedures, margins are normally still very high. For a market leader like Swiss listed Straumann, they run around 25% operating margins and almost 20% Net Income margins. ZimVie is not there at all in terms of margins currently but this is sticky business and with a good product offering as ZimVie seems to have I don't see any major reason why this should majorly deteriorate going forward. Listening to interviews with dentist who choose ZimVie's products it's clear that you get used to a set of tools you work with and the barrier to change to a competitor is high.

Spine

The global spinal implants and surgery devices market will witness a robust growth to 2030 with a CAGR of 4-6% depending on which research you choose to believe. Current market size is around $12 billion and there are a number of larger players in this field. Lately two large players Globus and Nuvasive have decided to merge and create the absolute giant in this field (combined MCAP almost 10bn USD). ZimVie's spine business is very USA concentrated, and as ZimVie has been for example moving out of the Chinese market, it is getting even more US centric.

The spine surgery market products can be divided into two main categories:

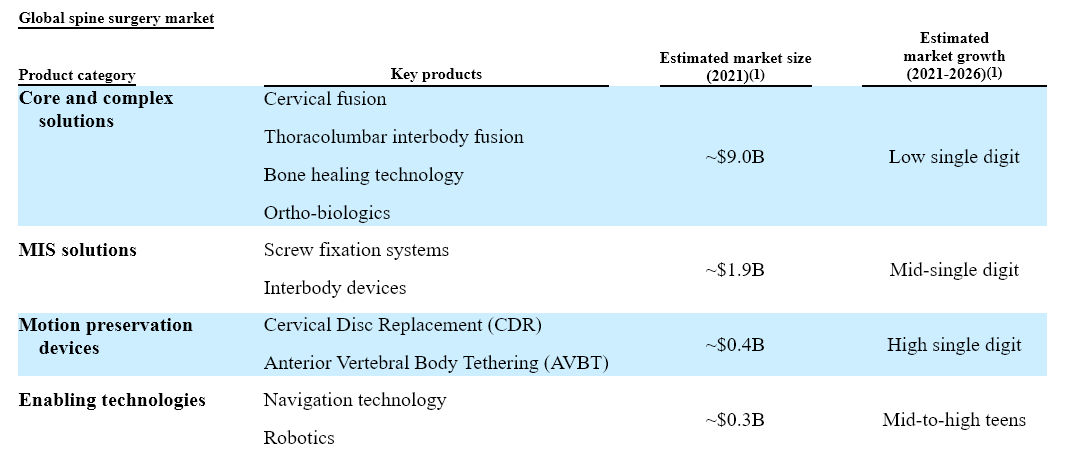

Fusion - The gold standard for decades where surgery outcomes have gone from terrible to acceptable over the last 2-3 decades. Fusion means fusing the bones in and making a segment entirely without movement. This is the majority (75%) of the $12 billion spine market with roughly $9 billion spent here.

Motion preservation - The new technology which for many years have been touted that it should take over from fusion. But for many reasons, including insurance coverage, doctors reluctance to rely on new unproven technology and actual issues and failures of surgeries using the new techniques have hampered the growth foreseen only 5-10 years ago. Another issue is to find suitable candidates, many older patients are not candidates for this new technology. Here my previous analysis on spine problems (us looking down in our phones all day) explains how a new group of younger people will need neck and back surgery. To conclude months of reading, ADR is superior to fusion for long term outcomes with lower re-surgery rates, especially for younger (below 60 years old). Currently Artificial Disc Replacement (ADR) is only 5-6% of the overall spine surgery market. ADR is expected to out-grow the overall market with a CAGR of about 12%.

I should also mention there are also other spine surgery procedures that make up the rest of the market, where ZimVie is also providing products.

Motion preservation leader

ZimVie owns one of the most used ADRs on the market - the Mobi-C. It has one of the longest track records and one of the most studied disc replacements that are still modern enough to be sold. It also is one of few ADRs to be fully FDA approved and approved for two level surgery. It is no longer the latest generation of ADR, as there are newer more advanced ADRs by now but the track record and FDA approvals puts in a strong position. It's easy to get lost here and think, well there are newer better ADRs on the market, Mobi-C is not attractive anymore, well yes and no. Because the competition is not really the other discs which share the 5% market share of the overall market. The big deal here is ZimVie manages to upsell a doctor who today does fusion and move him to do ADR on the patients. So to move the 75% of the market from fusion to ADR is where the big money is. This is happening but at a fairly slow pace, hence the 12% CAGR instead of the market overall of roughly 5% CAGR.

Like I mentioned in the intro, in 2016 Zimmer Bio acquired LDR Holding for about 1bn USD, with the flagship product being Mobi-C artificial disc. In 2016 the hopes were still high for a much higher growth than 12% for ADR, so valuation for owning these products have perhaps come down a bit, but it's worth to put into perspective that ZimVie's current Enterprise Value (EV) is less than what was paid for LDR Holding.

"Fun fact" - Elon chose Mobi-C. I just want to make clear for the reader (on Elon's twitter comment below) who is not into the details of neck surgery. That the first surgery failed for Elon has nothing to do with Mobi-C. He most likely had a bone spur in an area which is very close to arteries and his spinal cord, so to remove to spur has a small risk of creating serious damage or death. Obviously if the bone is not removed it doesn't matter how good the disc is, the spur has to go before you can recover from pain.

https://twitter.com/elonmusk/status/1317274309186838529?s=20

One should also mention the Tether device, which is targeting a smaller market but oh so important, as it is for kids with severe scoliosis in their spine. Again the current gold standard is fusion and tether is not a perfect alternative but it gives the kids a chance to keep their mobility in their spine. Given that we talk about kids and making their spine immobile at such a young age, even just investments aside, that ZimVie takes this product to market is major kudos to them. Hopefully ZimVie will also make good money on this in the future. Talking to a spine surgeon again he was not convinced that Tether gives better outcomes than Fusion, but doctors are strange creatures, they define outcomes differently than we do. They think more in pain scores and less in quality of life, many parents push hard for that their kids should keep their spine mobility and get the Tether device. Actually the story is similar with the ADR, it's very much patient driven, with patients seeking up the few doctors that does disc replacement instead of fusion.

Spin-off troubles, turn-around and potential offer?

Spin-off

Anyone picking up ZimVie's stock graph and looking at it from listing will be wondering, what kind of shit-show happened here. The short answer is that Zimmer Bio loaded ZimVie with a bit too much debt, just when FED decided to start a massive rate hike cycle. When I started to write this post, ZimVie stock had just experienced a -40% day after it's Q1 report and I saw a bargain trading at 7-8 USD per share. Since then the stock rallied which further lowered my interest to finalize my post (as there is less margin of safety).

To fully explain the pressure the share came under it was multiple factors:

The mentioned debt load worried investors, although the rate ZimVie pays is actually very attractive, only 1.5-1.75% above SOFR benchmark.

Bad results for ZimVie who still were struggling to form its own company and detach from Zimmer Bio, we have still not seen a fully clean result in my view. Q1 was promising and Q2 coming soon will be very important.

Mostly in my opinion it was the strange structure where Zimmer Bio left a 20% ownership which they intended to sell in chunks as ZimVie was listed. This seems to have happened through forward contracts to different funds and hedge funds and there was no end to how much the stock could fall while Zimmer Bio was still on the sell side. This created an insane double pressure on the stock, from both Zimmer Bio themselves and all the other Zimmer Bio shareholders who now got a small cap holding that does not fit their investment mandate (this is more the classical selling pressure from spin-offs which many try to take advantage off). As mentioned from what I can see from filings the 20% owned by Zimmer Bio is now sold and ZimVie has been listed long enough so those large caps funds have reasonably also sold now.

All in all this created an extreme opportunity in a slightly bruised company with a bit too much debt to plummet down to almost below 150m USD MCAP at it's worst. Incredible given the two quality business it owns. I unfortunately bought my first shares before the -40% day, but at least picked up enough guts to add and double my position in the 6 USD range.

Turn-around?

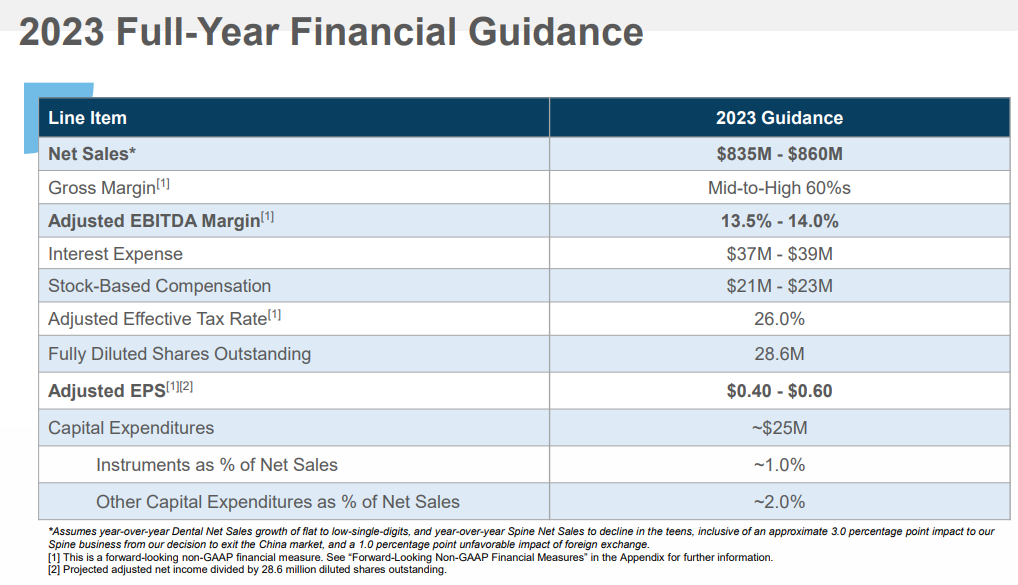

So is ZimVie turning around financially now? Well a bit early to tell, but Q1 was the first report that showed some type of possibility to move in that direction. Basically it stopped becoming worse and together with a quite bullish guidance for the rest of the year. The company needs to continue to show sequential improvement over Q2 to Q4 for the guidance story to be believable. The positive is that the dental business has stabilized and is not decreasing anymore. The spine business is still struggling, but mostly this is a one off effect of exiting China. Even if international sales continues to decline for Spine, this is so small now so it won't hurt the company as much anymore. Spine is really a US story.

Potential offer?

Lately the stock is up a lot off rumors' off a potential bid for whole or parts of the company. This makes sense to me for multiple reasons:

Buying the whole company because it's just undervalued, in the right hands this company is worth around or even more than when ZimVie listed, meaning 30-40 USD per share.

Selling either the Spine or the dental business makes sense to ZimVie, because the synergies between the two is almost zero. The only reason they were bunched together was because Zimmer bio wanted to get rid of two divisions that became oddballs in their company. It did not make sense to bunch them together. Now when ZimVie is struggling under a quite high debt load, selling one half and perhaps become debt free, with the other half left would make sense. As a shareholder I strongly prefer that the Spine business was sold as the dental business in my opinion is of much higher quality. The spine business has great long long term potential but it needs the stamina and right company to go through the growing pains until a product like Mobi-C is part of the new gold standard, we might be 10-15 years away from that happening. If the dental business was sold and ZimVie just left with the Spine business I would potentially sell my shares as I'm more interested to hold the dental part of this business.

The question then is who could the buyer be? Well we have seen a lot of shuffling around especially on the spine side. It could be anything from a Private Equity company to one of the other players who sees an opportunity to grab very strong products at a bargain price. Developing something like Mobi-C and getting it FDA approved costs hundreds of millions of USD. On top of that to build a track record of hundreds of thousands of implanted devices, with over 10 years of data, this is not something you can replicate. ZimVie is sitting on a gold mine with Mobi-C waiting for the US market to wake up to disc replacement surgery. The main reason US is behind the rest of the developed world in this area is due to insurance. This is coming around lately so now its a question of the doctors acquiring the skills to do these procedures. I expect strong movement in the US market over the coming 5 years. Some clever buyers might see the same thing. Zimmer Bio paid 1bn USD for the spine segment, if a buyer can get it for 5-600m USD and wipe out ZimVie's debt, that is a bargain price. Another way to value the Spine segment would be to look at listed Orthofix, which has also struggled although they have a good FDA approved alternative. Their EV is about 800m USD and I don't think ZimVie's spine segment should be worth much less than Orthofix (very similar total revenue, product portfolio etc).

Conclusion

Normally I would add some DCF here, thinking through valuation more properly, but as the stock now has a potential bid on it, I felt that it was more important to get this out, then wait another few weeks. There are many ways to value this company but this might be a rare case for me where DCF adds little value. I do see the stock being worth around 15-20 USD conservatively with a DCF, with blue sky around 30 USD. This becomes less relevant if ZimVie sells all or parts of its business. The bigger story here is that this company has great assets which are impossible to replicate, others in the industry must know that. Shareholders seems not really have understood that yet, that's why I'm very long ZimVie here, its my second largest position and after that gut wrenching -40% day and me adding at the bottom I'm in a very good position at the moment.

I'm holding on to my shares, hoping for a good outcome from the bid and especially a Q2 report which should continue to show an improving trend. Let me know what you think, happy to discuss in comments or on twitter. This was not one of my more well written posts as it was a bit rushed, I hope you can see past the spelling mistakes and poor sentences. But I can promise you this is one of my most well researched cases, especially Spine, but also dental.