OssDsign - USA bone regeneration pureplay

Post is originally from my previous blog www.globalstockpicking.com

Introduction

Neck and spine problems will be on the rise in the future. We stare down into our smartphones all day and spend too many hours sitting (with bad posture) in front of our computers (old post for more on this link). OssDsign has a very interesting product, in a small but important niche of this market. The product has high gross margins and is used in spinal fusions.

In short:

Market Cap: 630 MSEK / US$60m

Explosive Growth: Newly launched bone graft product (My estimate 100 MSEK run-rate in sales)

High margin: Gross margins should be 80%+

Large total market: Total market estimated above 1.25bn USD for USA only.

In this same spine space, I have taken a position in Zimmer Biomet spinoff ZimVie, which is targeting the newer technology of disc replacement. OssDsign is trying to bring innovation to the old and current gold standard of care, spinal fusion. OssDsign believe so much in their newly launched product that they are willing to close their previous main business line and fully focus on the new. At the same time, in a poor market environment for micro caps, the company managed to raise a substantial amount of cash from investors. Even more impressive was that this direct share issue was done around the current share price, so dilution happened at quite "fair" levels for existing investors. The product has 80-90% gross margins and has potential to be used in a large number of surgeries. All-in-all this is a high risk, high reward case where the odds of bringing this product to market is much higher than for Pharmaceutical products as there is no need for Phase 1/2/3 studies to launch the product.

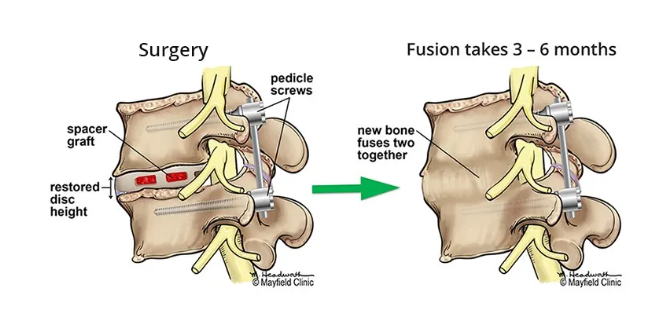

Spinal fusion

Spinal fusion patients are usually in tremendous pain and have often suffered for many years before a surgery is decided as the last option. Fortunately like many medical procedures, spinal fusions success rates have increased tremendously over the past 30-40 years and evolved from one of few bad options to the gold standard of care. Due to poor results of this procedure in the (far) past, it still has a quite bad reputation. The Spinal fusion procedure can simplisticly be explained as to remove the disc between two bone segments and then trigger the two bone segments to grow together (fuse) into one solid segment. Except the surgeons expertise in performing the steps of surgery, the most crucial component for the success of a fusion is to get as high confidence as possible that the full fusion will happen. Although outcomes have improved a lot over the years, that the fusions does not happen or partially happens, is still the weakest link of this surgery.

This is what OssDsign is trying to solve with their Catalyst bone graft material, where the idea is that the graft fills the void of the disc and triggers bone growth. The product sells at an ASP of about 2500 USD and depending on surgery different volumes of the product is needed. Together with two main competitors OssDsign have a bit of a first mover advantage here in a new generation of products coming to market increasing the interest from doctors to move to a synthetic solution instead of the other options available to them.

Although hard to exactly estimate, around 500 000 spinal fusion surgeries (lumbar and cervical) are done each year in the US. So with some quick math's of 2500 USD of OssDsign product per surgery the market size OssDsign is competing for is about 1.25bn USD. With an aging, obese population the number of surgeries just keeps growing. Given the rapid increase of spinal fusions, a both efficient and cost effective solution for creating stable fusions of the bone is highly desired by surgeons. As a small company out of Sweden, it might seem far fetched that they would win the US market. But together with 2 other players (where one is also a small company) they are the only ones seeing FDA approvals and all indications so far seems positive towards a chance to win a decent market share in this segment. The upside for OssDsign even at 5-10% market share is very substantial as this is a high margin product. Let's try to dive deeper into this topic.

History

OssDsign listed in 2019 for 27.5 SEK per share and today it trades around 6 SEK per share, not a great outcome. What the company has done historically is unusually irrelevant though. The company you are purchasing as of today, is vastly different to what was listed in 2019. How come the company has changed it strategy so drastically and quickly? OssDsign listed as a 3d printed cranium implant company with a titanium-reinforced calcium phosphate plate. I don't think the company necessarily done anything wrong in launching this product into the market, the problem, I believe, is that its just too niche. Yearly sales have roughly doubled since pre-IPO from some 20 to 40 MSEK. Although it could probably scale further, there is not enough patients in need of these type of cranium implants to really deliver shareholder value from this one product. In the hot "free money" era, OssDsign then decided to expand its produce range by an acquisition. OssDsign recently announced that they will abandon (in best case find a buyer) the cranium business and fully focus on their spinal fusion product Catalyst (which was the acquisition they made). Below is a timeline of the Catalyst product. Press read more..

Timeline of OssDsign Catalyst

2020: In the "free-money" era OssDsign purchased a British company (SIRAKOSS) for 8.4m GBP in Nov 2020. In the purchase price is also a low single digit royalty fee to the original founders. Given that this is a very high margin product I don't see an issue with the royalty. SIRAKOSS was basically only setup to launch their invention called Osteo3 ZP Putty which OssDsign later has relabeled as OssDsign Catalyst. As already described in the intro, this type of product has a much larger addressable market. The SIRAKOSS team was the two gentlemen below, working at University of Aberdeen in Scotland. Already at OssDsign's purchase SIRAKOSS had received FDA approval of the type 510(k) to use the putty in certain indications: ZP Putty FDA approval.

Source: https://abdn.ac.uk/stories/pioneering-new-bone-graft-material-to-improve-patient-outcomes/

"The culmination of the team’s research was the development of a brand new silicate-containing calcium phosphate material with properties much closer to the mineral crystals found in real bone than had been previously achieved in any other synthetic bone graft material. By processing the material to have smaller crystal dimensions and notably smaller pores than other synthetic solutions, the material achieves a much higher surface area, with the result that the surface supports bone repair more effectively and is more readily remodeled than traditional ‘ceramic’ substitutes."

2021: As a small company OssDsign decided to try to focus on the US market and have worked together with a smaller number of spine surgeons to evaluate the product through the trials they kicked off. The product was initially launched in late 2021 in the US. In late 2021 the first small scale study, called "TOP FUSION" was also launched, this study was only recruiting 17 patients and was run out of Budapest.

2022: Early 2022 they got an approval for their first "real" US based study called PROPEL, they started to recruit patients and reached a 100 participating patients earlier than expected before year end 2022.

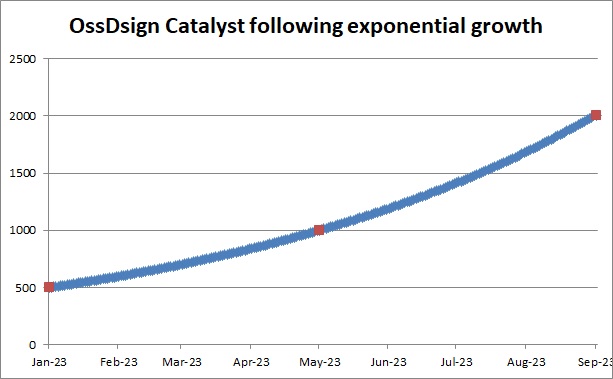

2023: Early 2023 the first results from the "TOP FUSION" study was published, which showed a good outcome. The PROPEL study was successfully fully recruited with over 200 patients. After this things started to move very fast. Although the study had only about 200 patients a few weeks later the company announced that 2000 patients had been treated with OssDsign Catalyst. So the product has been used quite extensively outside the study by a smaller group of surgeons.

To illustrate the growth of total procedures in 2023, it's better to show a graph:

The company is pointing to IDN contracts (network of healthcare centers) as the reason for the recent strong growth. But there is more to the story here in my opinion. My own interpretation of what has happened is that spine surgeons that were early users of the product saw good results (although these are to large extent not published yet) and started to use it more widely. It raises in my view the probability of successful results in the PROPEL study. Doctors would not keep using it in surgery 3-4-5 if the outcomes were not good. This is basically the bottom line why I invested in the company. The week after announcing strong sales growth the company received another clearance from FDA for usage of Catalyst in a new indication (interbody cages).

Drastic strategy shift

So with all this happening and sales from the Catalyst product has gone from zero to twice the cranium business within the span of literally two years the company decided to make a drastic shift. OssDsign then made the "brave" announcement to fully focus on the US market and becoming a pure play orthobiologics company, which for now means betting all on the Catalyst. With this announcement they also attracted 150 MSEK (13m USD) in new funding through a direct share issuances. The Swedish micro/small cap space is in a proper bear market currently and to get this issuances done roughly at the current market price of the stock was in my view very impressive. Money will be used for costs of launching the product more widely in the US, as well as finalizing the very important PROPEL study with over 200 participants. This was the second factor which made me invest in this company, funding secured is important in this environment.

US spine market

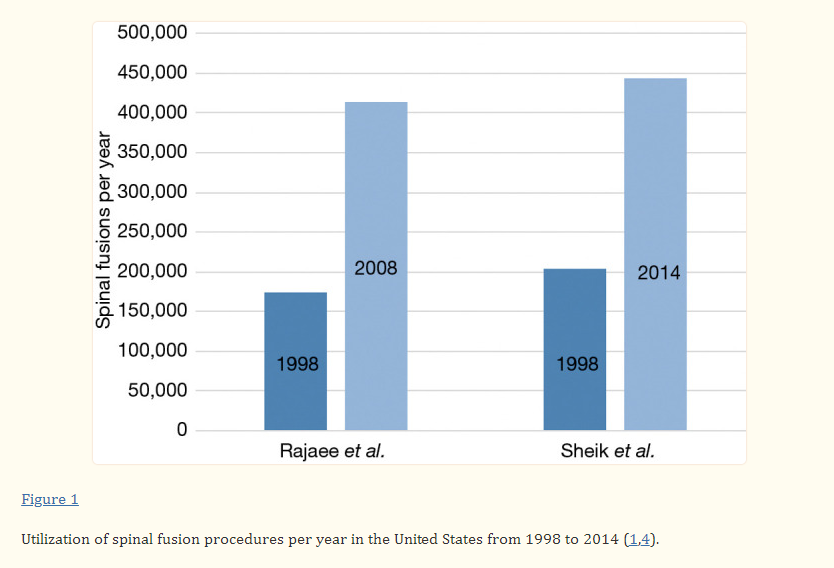

As OssDsign is fully focusing on the US market for their Catalyst its interesting to look at how that spine surgery market developed over the years and what the outlook is forward. As mentioned an estimated 500k spinal fusions is done each year in the US. Some other quote this as high as 650k fusions (Source) I found the below journals confirming not only that 500k is a decent estimate (given 440k in 2014) but also showing how extremely rapid the growth in number of surgeries has been during early 2000's.

Source: https://www.ncbi.nlm.nih.gov/pmc/articles/PMC7797794/

I would expect the growth in fusion surgeries to decrease quite significantly and rather stabilize, as some segments like cervical fusions will over time now be replaced with artificial disc replacements. Like explained in previous post about ZimVie, there is still something like 8 times as many fusions compared to ADRs done in the US. That the market does not massively grow from here is less of a problem for OssDsign as the big question is what kind of market share could they get. Nevertheless the US spinal fusion market is still expected to grow with a CAGR of 4.6% per year until 2032 which is a further nice tailwind to the case (Spinal Fusion Devices Market Expected to Grow at 4.6% CAGR).

Existing technologies

Although the early evidence and especially uptake from some doctors tells a story that OssDsign struck gold with their purchase of the Scottish University company, they are of course not the only company globally that has tried to solve the problem of improving fusion outcomes.

Gold standard is your own bone

The current gold standard to trigger bone-growth so that the bones fuse, is to use your own bone, grinded down into smaller pieces. The problem with this is obviously that where do you take this bone from without causing harm? Sometimes the surgeon can take a little bit of bone from the surgery location, a bit of the bone can be sacrificed there as the segments anyway will be fused. Most often this is not enough and then there are a few options how to create the bone graft:

Take bone from the anterior iliac crest, this is deemed the safest place on the body to harvest bone. Although it's the safest place, its still not without it's problems, its a surgery so there is always an added risk of complications (infection etc). A quite high number of patients have short term and some even long term pain or sensory disturbance from the donor area. This type of procedure is also called an autograft - Further reading on problems with harvesting bone.

Take bone from a cadaver (i.e. a dead person), this bone needs to be properly cleaned and processed through different processes. This is sometimes sold in the form of Demineralized Bone Matrix (DBM). Again there are some tail risks with this and also that this bone is after the cleaning process is not as effective to trigger bone growth as your own bone. This type of procedure is also called allograft. This is often also mixed with own bone, so a combination of iliac crest bone and DBM which is again sold by a number of companies and is among the cheapest options, around $1500 for a DBM for a fusion.

Use only synthetic products like the product OssDsign is providing, there are multiple other materials on the market (I will mention some of them below).

And lastly what in my view seems to start to emerge as the new gold standard, mixing your own bone with a synthetics like OssDsign Catalyst. This gives the confidence of triggering fusion from using your own bone and mixing it with something that even on it's own would be a decent material to trigger bone growth. Mixed together say 50/50 it has in the early studies not only for OssDsign but also other brands products shown promising outcomes. The benefit here is that if you are lucky you can skip the harvesting from the iliac crest or remove a much smaller amount of bone from the iliac crest.

OssDsign Catalyst

Looking at the outcome data for OssDsign Catalyst from a pure scientific results perspective is hard. Initially I thought these products would need to proven with scientific data to by cleared by FDA. I learned that the 510(k) clearance is much easier to achieve than a phase 1/2/3 full FDA approval process. Essentially the Catalyst and previous products like Attrax are all approved based on a predicated product, meaning an earlier product which they claim equivalence against. From my understanding no further evidence is needed that proving that the product is close enough to a previously approved product to get the 510(k) clearance. OssDsign CEO is in certain interviews mentioning how they done something very special to get the FDA approval, how they belong in an exclusive group of products which have the FDA clearance. I'm sure it's still hard work to get the clearance but not nearly as hard work as passing FDA Phase 1-2-3 studies to get clearance. Due to FDAs treatment of these type of products its possible for a very small company with limited means to bring the product to market. Perhaps that is FDAs intention.

Rabbits

The existing published studies of Catalyst is first in a rabbit study published early 2021 in the Spine Journal. The study shows that the rabbits have successfully fused with the Catalyst substance. Even if it was a rabbit study the number of rabbits used was low and I personally put quite low significance on this study.

Safety Study

A safety study was performed on the roughly 500 first use cases of Catalyst in humans. The outcome of this study was very good with all complications seemed to be unrelated to Catalyst itself: Safety study.

First fully studied case

Out of the small PROPEL study the first (human) case results was published, showing a good outcome at first use: Link to study.

Conclusion on product quality

All of the above is necessary basics steps to launch the product and build up the credibility that the product works. But given that 2000 patients have been fused with Catalyst, there are clearly many doctors out there with much more information on the Catalyst than what has been published in studies. I tend to trust the 2000 procedures more as a stamp of approval that outcomes seems to be good/satisfactory. Another important aspect is that handling of the bone-graft is easy. Not all products are as easy to use (stay in the right place etc). Small things like this might in the end mean a lot for adoption rates of a product.

Competing products

So trying to understand this landscape of products is quite complex. But basically all products are shooting for in the best case #3 above, to fully replace your own bone with a perfect synthetic product. That's the dream scenario, create a synthetic product which in 100% of cases always triggers bone fusion in the patient without need of anything else. Realistically most products shoots for being a filler, to mix out with own bone but hoping to convince surgeons to use it without mixing.

Three different type of synthetics are competing for the future of bone graft materials:

New generation materials with nano-structures that imitate how are own bone looks like at nano scale - OssDsign Catalyst belongs to this category, also Attrax and MagnetOS which I will mention below.

rhBMP-2 (recombinant Human Bone Morphogenetic Protein-2) - Phew that's a complicated word! This is a highly potent protein which is expensive to produce. The large medical players produce this for a cost of around US$3500 per fusion. This has been the go to product when surgeon suspects that patient will struggle to fuse (due to age, obesity, smoking, etc). The problem with the product is that it can also trigger bone-growth where you don't want it, creating bone-spurs which creates new problems of nerve impingement etc. The product is for sure still used quite extensively, but listening to conferences among surgeons, I can feel they would prefer a better option with safer outcomes.

P-15 peptide enhanced graft - P-15 is a synthetic, 15-amino-acid residue found in type I collagen, containing the potent cell-binding domain of collagen. This can be adsorbed onto a calcium phosphate substrate and will enhance cell attachment and extracellular matrix and factor production, resulting in the formation of bone. Although no product is fully launched on the market, recent studies show superior outcomes of P-15 versus rhBMP (see study) The leading company in this area is Cerapedics, which is going to trials to prove the outcomes of it's iFACTOR P-15 peptide.

It is hard to define what is a competitor, as there different fusion techniques which give different synthetic materials with different properties an advantage. As a basic example a lumbar spine fusion can both be done from the back or go in through the front (stomach). Two different approaches with their drawbacks and benefits. Further the fusion can be done with screws and fusion material placed on the sides, or a cage can be placed between the bones and the cage is stuffed with bone graft. The cage can be fixed, or even expandable, which again gives different textures of bone graft advantages. To summarize, it's complex to create one bone graft product that wins in all situations. But a good product which fuses as well as your own bone, will probably be a strong candidate in many surgeries. As long as the surgeon can work with the texture (so it for example does not float away like a tooth paste) and fusion rates are high, it is already a strong candidate in the market. OssDsign Catalyst has the right texture, this is an important point of the quality of their product.

Looking in more detail at competitors

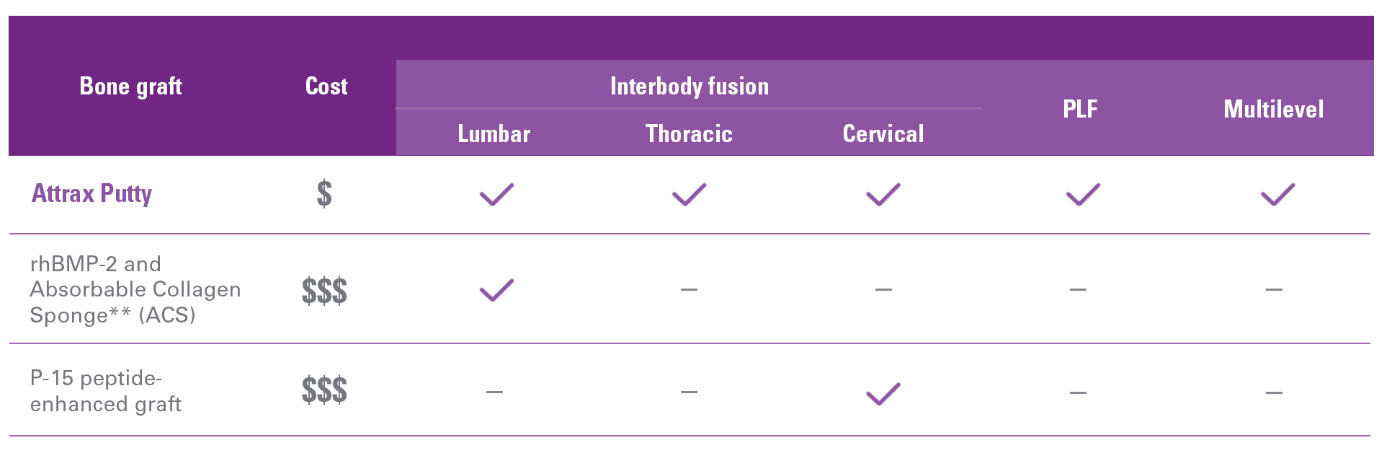

OssDsign is currently charging in the range of 2000-2500 USD per 10 ml and from what I can find Attrax Putty costs about $1200 USD for 10 ml (quite normal amount used)

Estimates vary but rhBMP costs around $3500 per level of fusion done.

P-15 peptide cost is more un-clear but should be in the same range as rhBMP.

The competitors that stand out to me are (both belong to listed companies):

Nuvasive/Globus - Attrax Putty

Kuros Bioscience - MagnetOS

Nuvasive's pitch for Attrax below:

Since Attrax is sold by a larger company, they have had the financial muscle to do multiple studies in different type of procedures. Although as described above the FDA 510(k) clearance does not require randomized trials with A/B cohorts, this is of course a clear positive to have when trying to convince a surgeon to use your product. So Attrax has a number of these type of studies which have been released over the past years. This is clearly a big benefit to Attrax vs all competition that does not have such scientific data to lean on. The negative is that I do believe Attrax is less advanced in its micro-structure compared to MagnetOS and OssDsign Catalyst, I don't have any solid evidence to back this up except the below:

There is an interesting history with Nuvasive and Attrax, as it was created by the lead man of Kuros Bioscience Joost de Bruijn. Joost has been one of the true pioneers in the field of new generation synthetic materials. Already in 2009 he sold his company and the Attrax product to Nuvasive in a 80m USD contract: Link to source. It took Nuvasive a number of years to launch the product they got FDA clearance and launched the product in early 2016: NuVasive Launches AttraX Putty.

MagnetOS

How come Joost de Bruijn is linked to both of OssDsign's competitors? Kuros Biosciences is the only true small cap competitor to OssDsign in my view. In 2000, it spun out from ETHZ. In January 2016, Cytos Biotechnology and Kuros Biosurgery Holding AG (“Kuros”) merged to create Kuros Biosciences. In early 2017, Kuros acquired Xpand Biotechnology to improve its orthobiologics portfolio through the addition of the MagnetOs product. The same Joost de Bruijn was the man behind Xpand and this was his second time to sell his product to a larger player, and from what I can see they were handsomely paid as Kuros paid some 2 million shares with Kuros at the time trading at 16 CHF per share (source).

If one just looks at the above history, Joost de Bruijn seems to have been the mastermind milking the market twice on this product. I do believe he tried to improve and differentiate the MagnetOS product from the Attrax product he previously created (after all he had many more years of experience when creating MagnetOS). Joost is also still active in Kuros and seems to have kept many of the shares he was given in Kuros when selling his company (1.1 million shares held). He could have taken his money and ran but he is trying to make MagnetOS successful. So my conclusion from this is that Attrax is the competition in the lower price segment, with the large Nuvasive/Globus spine company behind it. But from a technical and surgery outcome quality point of view, MagnetOS is the real latest generation competitor. MagnetOS has also come further in the adoption of the product, according to Kuros it has been used in 15 000 spinal fusions so far, already in Aug 2022 they reached 10 000 fusions, so the adoption rate of OssDsign Catalyst is not far behind MagnetOS.

Which one is better MagnetOS or OssDsign Catalyst? I don't know and probably nobody else either. We need to see more data, more adoption of the product to deduct a clear winner. And probably since there are so many surgeons operating in different ways and different procedures done there is no magic bullet that will always be best. I find the story about Joost compelling enough that I might (if you are lucky) write that up some day also. Until that day here is an initiation report of Kuros: Kuros Bio

Management / Ownership

CEO is Morten Henneveld with a background in sales and restructuring. Most relevant experience was as VP at Zimmer Biomet Spine division until 2017, meaning he is an old colleague to the team I'm today invested in through ZimVie. Although he worked in fairly US centric Zimmer Bio his area of focus was EMEA, so his knowledge about how to penetrate the US market is possibly limited. This is the first time for Morten to step up into the CEO role as in his latest position he was a SVP for Danish hearing aid company GN Group which is a mid/large cap company.

An interview with Morten here: Link

Other interesting names on the management team is Tom Buckland who seems to have joined through the SIRAKOSS acquisition. Tom has previous experience from bone graft companies as co-founder of ApaTech which was purchased by Baxter for 330m (Baxter - Apatech). In the same deal the VP of Sales US - Eric Patermo also comes with a background at Apatech. This is a bit similar like the Kuros Bio situation where the same names again come up in the sector. To have these two experienced gentlemen onboard I see as a positive for OssDsign's likelihood of success.

The shareholding from the management is very modest in outright shares, the CEO only has 200 000 shares but all of management are incentives through subscription options which is more substantial, for example 2.3m shares for Morten. It would have been nice to see a bit more skin in the game and perhaps some insider purchases either through or after the recent share placement.

In the recent direct share issue TAMT AB, Karolinska Development, Adrigo Asset Management, Lancelot Asset Management and Linc AB were the takers.

Valuation

Due to the explained competitive landscape it's in my view not realistic to believe OssDsign Catalyst can win whole or close to the whole US market. A slam dunk outcome would probably more be in the range on 20-25% of all spinal fusions. More than this is not needed for the case valuation wise. Already at 10% market share we are talking about 50k procedures with US$2500 in sales, that translates to 1.3bn SEK in sales with 90% gross margin and probably 20%+ net income margin vs current MCAP of 630m SEK.

I like to draw up scenarios in a DCF analysis for more mature stocks but find such an analysis pointless at this stage of the company. I draw comfort from the capital raise, but would still expect another capital raise before the company can reach a cash flow positive stage. This depends if they team up with a larger company in their distribution or not (currently no plans for that). Again here noting that Kuros Bio with MagnetOS has teamed up with a larger player. Another way to look at this are the numerous purchases from larger firms in this field. It's not unlikely if OssDsign Catalyst continues to sell well in the US market that a larger player just puts in a bid for their product.

Market share model

Another way to play with valuation is to look at what kind of market share of the 500 000 yearly spine fusions that Catalyst can win. If one does the "silly" exercise of modeling current growth to the non-linear function it's currently exhibits, the extrapolated growth would mean a 5% market share (25000 use cases) already by end of 2024.

If one rather looks at MagnetOS and their growth rate, it seems plausible that OssDsign (with continued good clinical outcomes) would sell some 5000 Catalyst during 2024, meaning 1% market share (if one catalyst is used per surgery). Making some quite conservative assumptions about further growth from that point on yields the following values.

This numbers are of course highly dependent on successful outcomes for the studies that OssDsign plans to present. Talking about that, since if something negative comes up along the way, the company is basically a zero. So this can in my view unfortunately not be sized as a larger position, but will stay a small speculative position until they are a more proven company. I also did not pen in the 4.6% CAGR of number of fusions done, at the moment this tailwind is of less importance compared to the market penetration by OssDsign.

Conclusion

To conclude this somewhat technical post. My take on this is that the previous generation of synthetic bone graft materials were not great substitutes for using own bone (autograft) or cadaver bone (allograft). But with the latest generation this is shifting and this is changing the landscape quite fast in favor of these few products like the Attrax, MagnetOS and Catalyst to win market share from previously used products. I can see a trend of these latest generation products mixed with own bone 50/50 as the new gold standard of usage. In complicated cases with obesity, smoking etc bone fusion is difficult at best. To have better options like these latest generation products will hopefully make a significant difference for patients and hopefully also save money where more complicated and more expensive solutions previously was needed (rH-BMP2 etc).

It is still up to OssDsign to play their cards right and pivotal will be results from their fully recruited PROPEL study. This will be an exciting case to follow during 2024 and Kuros Bioscience who is perhaps one year ahead of OssDsign is rallying strongly on the Swiss exchange in the past months. If that is any guidance for OssDsign's 2024 is yet to be seen.

Hope you enjoyed the reading and agree it's an interesting high risk small cap case to take into the portfolio at a small weight. As always do your own due diligence and let me know what you think!